It would be fair to say that the recent “mini-Budget” ended up causing somewhat of a stir in the markets.

A series of tax cuts, the reversal of both the National Insurance increase and a planned Corporation Tax rise, and an eye-wateringly large intervention in energy markets prompted unprecedented market movements and even a rebuke from the International Monetary Fund (IMF).

The announcement was swiftly followed by the pound falling to a record low against the dollar (although it has now recovered, somewhat) and a sharp rise in the interest rate the UK pays on longer-term borrowing.

The volatility also resulted in emergency intervention from the Bank of England (BoE) and a U-turn on plans to abolish the 45p additional rate of Income Tax.

It’s natural that you may be concerned about your finances in light of these events. So, read on as we cut through some of the more sensational headlines and focus on how the recent uncertainty may affect you.

A brief summary of recent events

- The recent mini-Budget caused volatility in markets, with a fall in the value of the pound and sharp rises in the cost of government borrowing

- The BoE stepped in to reassure markets, particularly with regard to cash calls on final salary pension funds

- To calm markets, the chancellor announced that the government were no longer going to abolish the 45p rate of Income Tax

- The mortgage market was thrown into turmoil as lenders withdrew products and replaced them with more expensive deals

- A weakened pound and high inflation may lead to further increases in interest rates.

If you’d like more detail on any of these areas, read on and you’ll find more analysis.

Of course, if you’re worried about current events please get in touch for a chat. We understand that, for many people, these events are unsettling and we’re here to help you understand what they mean for you.

When you’re faced with a sea of worrying news headlines, it’s very easy for your subconscious biases to take over. Making knee-jerk, emotional decisions may help you to feel “in control”, but these can often have a detrimental effect on your long-term financial security.

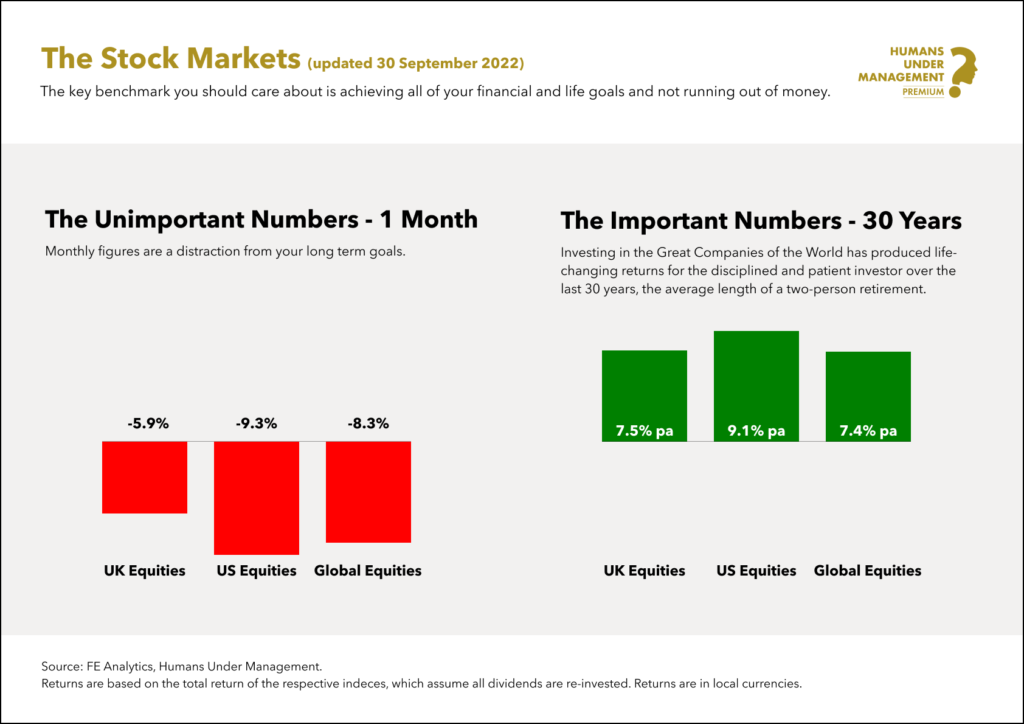

2022 has undoubtedly been a difficult time for investors but is important that we focus on the longer term and not just the present. The below image provides confirmation of the numbers that we believe are important for investors:

Comments on recent events: A falling pound and high inflation

One of the immediate consequences of the mini-Budget was that markets reacted negatively to announcements about tax cuts funded through borrowing.

Sky News reports that, at one point, sterling slipped by nearly 5% to a low of $1.0327. That’s an all-time low against the dollar, surpassing the previous low point set in February 1985.

A weakened pound makes imports more expensive, which could further push up inflation. In addition, interest rates often rise during periods of currency weakness to attract money into the economy.

It’s worth noting that, after the reversal of the abolition of the 45p tax rate, the pound rallied, returning to the level seen before the mini-Budget, at around $1.13.

The likely result of the weakness in the pound is that interest rates will rise sharply. Schroders expect the base rate to rise to 5.25% in the middle of 2023 – more than twice the current level.

That’s bad news for borrowers, but potentially good news for savers.

You will have seen the headlines that many mortgage lenders immediately withdrew their mortgage deals, with Moneyfacts reporting that almost 1,000 products were removed from the market in just a few days after the mini-Budget. Many of these have now been repriced at higher rates.

The BBC reports that the average rate on two-year fixed mortgage deals jumped to 5.75% on Monday 3 October, up from 4.74% on the day of the mini-Budget.

This means that anyone looking for a mortgage into 2023 will likely pay a significant amount more than before, and those coming off the low-cost deals popular over the last five years will see their repayments rise sharply.

In theory, savers should also benefit from higher interest rates on cash savings, but these have yet to filter through to the market in a meaningful way and with inflation significantly above the interest that can be earned, cash remains an unattractive option for the majority of medium to long term investors.

BoE action supported pension funds

It’s likely that you’ve seen some pretty alarming headlines over the last couple of weeks. The Telegraph’s “Pension funds crisis forces £65 billion bailout by Bank” is typical of the media reporting of the fallout of the mini-Budget – but it’s important to note that BoE action was designed to protect pension funds.

If you have a “final salary” or defined benefit (DB) pension

The recent sell-off of British government bonds (“gilts”) caused the rate of return the bond generates (the “yield”) to dramatically increase.

This affected defined benefit (DB) or “final salary” pension funds because the pension schemes typically invest more than half of their assets in bonds, in order to pay pension liabilities decades into the future.

To avoid being exposed to market volatility, these pension schemes typically hedge their positions through gilt derivatives managed by so-called liability-driven investment (LDI) funds overseen by major fund managers such as BlackRock, Legal & General, and Schroders.

If yields rise too far and too fast – as they did after the mini-Budget – the schemes need to provide more cash to the LDI funds because they end up paying out more money in the transaction than they are receiving.

The recent sharp moves prompted emergency calls for the pension funds to provide collateral, so they may only have had a couple of days to find this cash. This led to the headlines about the funds potentially “going bust”.

The BoE’s intervention – they stepped in to buy billions of pounds of British government bonds – calmed the market, as it gave pension schemes time to process transactions in an orderly manner to secure their positions.

What it means for you is that, as long as the employer sponsoring your pension scheme remains solvent, there is little risk of your pension not being paid in full.

If you have a “money purchase” or defined contribution (DC) pension

Most UK workers saving into a pension are members of a defined contribution (DC) scheme.

Although you can usually decide where your money is invested, the default option is typically a mixture of equities, bonds, gilts, and other assets. If you’ve checked your valuation in recent months, it’s likely that you have seen a fall in value – mainly as most developed stock markets have fallen in 2022.

If you have years to go until your retirement, there is plenty of chance for markets – and the value of your fund – to recover in the coming years.

Vanguard say that the average “bear market” in the UK – when values are falling – lasts for just over a year, whereas the average “bull market” – where prices are rising – lasts for almost six years.

If you’re nearer or in your retirement, it’s worth consulting us to determine the best way to draw income. We understand that it’s a tricky time, and we’re here for you.

Accessing income from sources other than your pension could improve the long-term sustainability of your fund.

Two reasons recent market moves could benefit investors

1. The stock market is not the economy

Firstly, it’s important to note that the recent turmoil hasn’t had a dramatic impact on stock markets, though the majority remain significantly down during the calendar year. The UK’s FTSE 100 – an index of the 100 largest companies in the UK by market capitalisation – fell from 7,159 the day before the mini-Budget to 6,893 at the end of September 2022 – a drop of around 3.5%.

Part of the reason for this is that more than 75% of the revenues of the largest 100 companies listed on the London Stock Exchange are derived from overseas.

In many cases, these profits will be boosted by the recent decline in the value of the pound. This combination of higher profits and lower share prices improves the attractiveness of UK shares and should lead to higher long-term returns.

Additionally, if you have a well-diversified portfolio, the rising value of the US dollar provides a positive contribution to sterling-based returns, as US assets are worth more. This has helped to shore up portfolio returns for many.

2. A fall in stock markets means the opportunity to buy “cheaper” assets

Legendary American investor, Warren Buffett, famously said: “Be greedy when others are fearful, and fearful when others are greedy”.

Many investors believe that it is good to buy at a time when stock markets are low. The principle is that you can buy more shares or units for your money, leading to a boost in profits as and when markets pick up again.

While it’s impossible to time the market, drip-feeding investments in an uncertain market is one possible approach. If the markets go down further, you’re buying at a cheaper level. This could help smooth out your returns, with the hope they recover and grow in the longer term.

Stay The Course

The immediate future remains uncertain, with more questions than answers. Central banks have a mandate to create long-term stability by dishing out short-term pain if that’s what they believe is required. This is a process for which there is no shortcut.

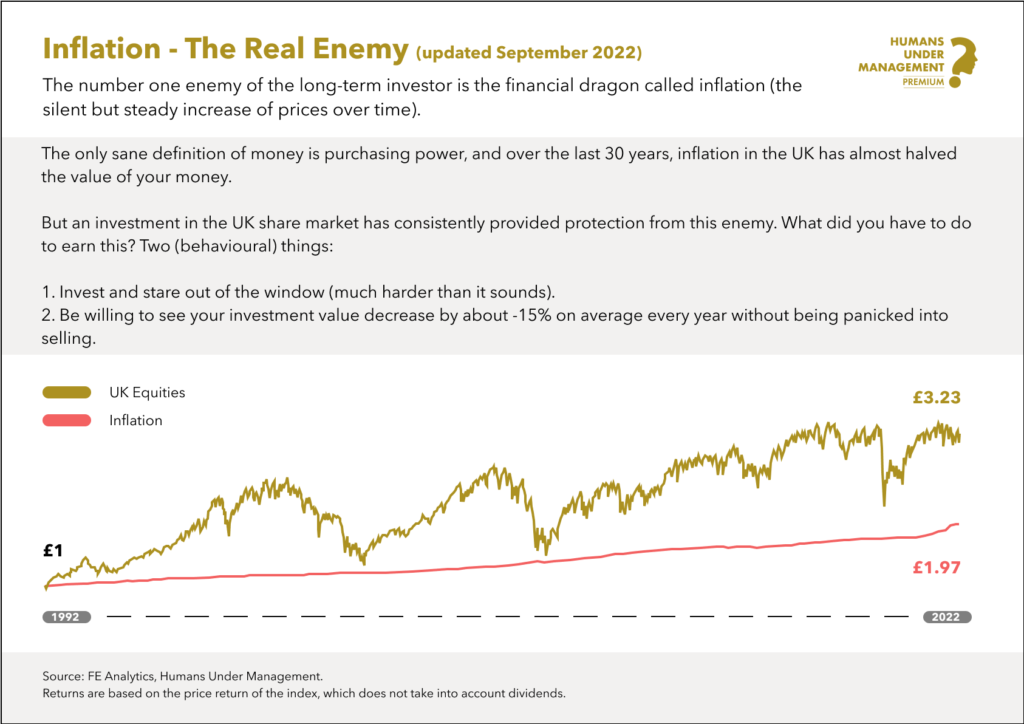

The exact path out of the current turmoil is unknown to every market participant, but given that we have our eyes on the long term, we have certain advantages. While, in the short run, the market will continue to be governed by the sentiment and emotions of billions of participants, in the long run we continue to remain confident that, as a group, the businesses that you are invested in will reward patient holders of their shares. We believe that this is the best way of protecting the real value of the assets you have built up against the enemy that is inflation.

Get in touch

If you’re concerned about recent events, or you’d like to have a chat, we’re always here to help. We can talk through your current position and the effect of the mini-Budget on your finances.

Please note

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future results.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates and tax legislation may change in subsequent Finance Acts.